How we rebuild our economies after the Covid-19 crisis will depend on how societies change their relationship with finance.

Several decades of financialisation have given outsized power to financial markets and actors. Financial systems should serve the productive economy and be controlled by societies, but with financialisation, the relationship has often been reversed, leaving societies more vulnerable in the face of shocks and disruptions.

Our research at IDS reveals where finance has gone too far, and it offers ideas for a better, more positive role for finance. A more restrained, humble, productive, and socially embedded financial system is what societies around the world need for sustainable recovery and global development.

Financialisation has gone too far

Taking stock of the past decade, it is clear that unfettered financial development has made us even more vulnerable to the economic fallout from the Covid-19 pandemic. The instabilities that produced the 2008 crash were papered over, while new ones have been built up with easy money unleashed by quantitative easing.

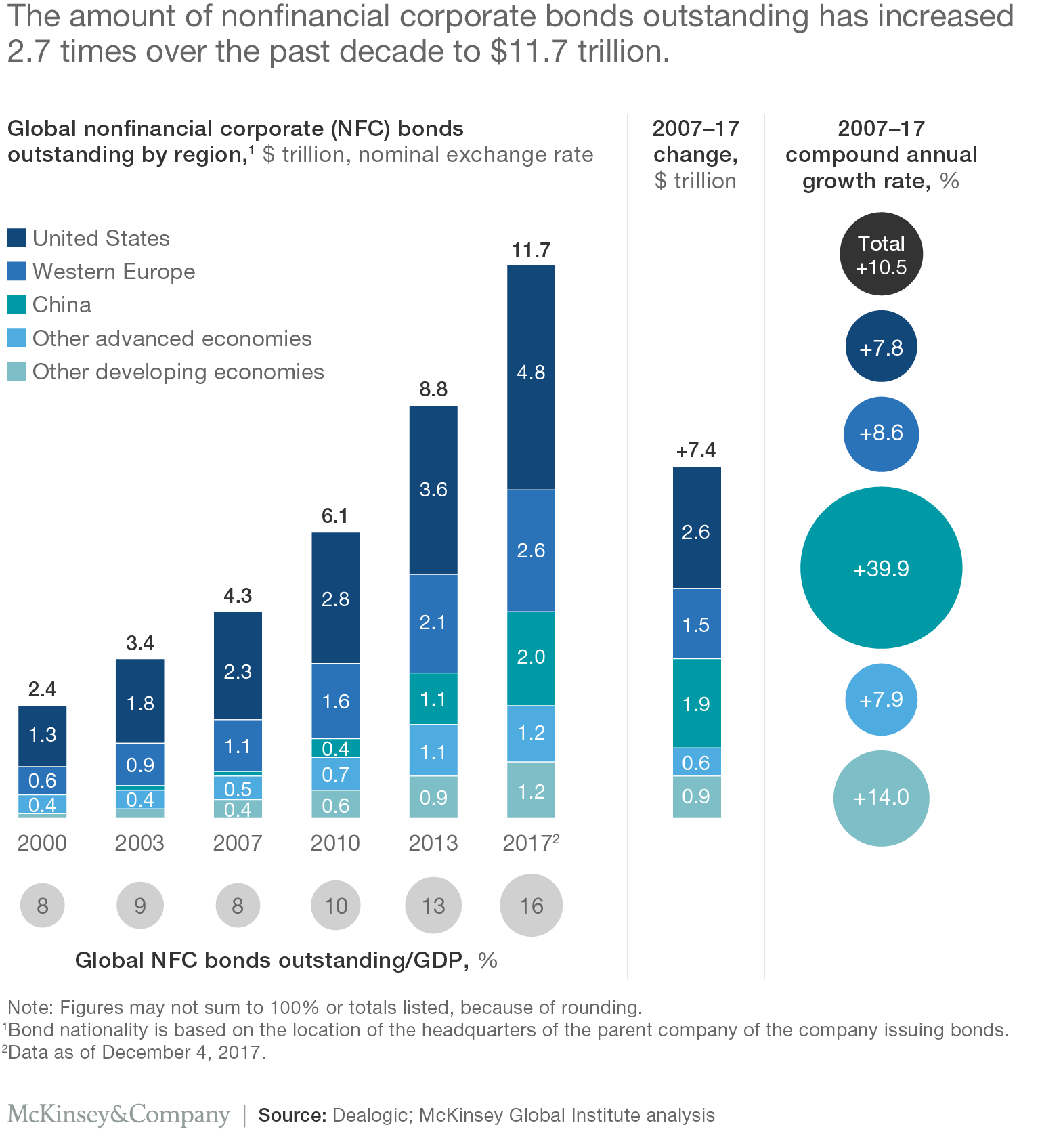

An enormous buildup of corporate debts, proceeding fastest in China and other developing countries, has emerged as the most likely trigger for a renewed collapse, which likely will deepen the impending post-Covid depression, which the current phony financial recovery might delay but cannot prevent. If, or when, the current debt bubble implodes, it will not be Covid-19 that is to blame, so much as years of political inaction towards making financial systems stable, modest and subservient to societal needs.

{kind=link}

Now, as last seen in the 2008 crisis, governments around the world are adopting ‘radical’ financial crisis management measures. Some of these, such as income support programs, dividend payment suspensions, and debt moratoria have a subtly progressive flavour. But policy elites are likely to regard such measures as expedient only in the crisis moment and return to pre-pandemic policies, which prioritise financial interests over social ones, in a financialised “recovery” which would exacerbate already staggering global inequalities. The virus and policy responses to it have made the richest even richer while workers have been punished even for asking for reasonable protections. The pandemic has also reinforced structural injustices linked to gender and race. Covid-19 is far from a ‘great equalizer’. A return to austerity would be a catastrophe, with more people’s futures ‘stolen’

Yet with political will, the pandemic could be an opportunity to ‘build back better’ by reasserting social control over finance, if we correctly diagnose the causes of financialisation and resolve to redress them.

Finance needs steering by a ‘visible hand’

Every type of economy and society needs some form of financial system. This does not mean a larger, less regulated and more powerful one is better. Rather, our research reveals the need for a more ‘visible hand’ in finance, to steer and control finance, and make it socially useful.

At the macro-financial level, stronger regulation is needed to prevent destructive boom-bust cycles from recurring. Unstable financial systems harm everyone, except for a tiny minority who can privatise speculative gains and socialise losses. Whereas governments in the last decades have mostly reacted to crises, they should instead place limits on financial expansion, limit the gains and losses, and channel finance toward the greater social good.

Another urgent task is to counteract the structural imbalances in international financial markets, which starve developing countries of the long-term investment capital they always need, and even more so in the wake of a public health emergency. Public development banks could play a major role in the post-Covid reconstruction, helping economies to structurally transform while rebuilding, if international financial institutions like the World Bank were to cease diminishing them as mere enablers of profitable private sector investments. Our research has shown that globally, development banks (including national, regional and global) already lend around $2 trillion annually, about 10% of world investment. If they were to increase their exposure by 20% this year and next, this would add $400 billion for investment in sustainable development, allowing societies to ‘build back better’ with more and better jobs.

Cross-border capital flows also can and must be controlled. The uncertainty brought by the pandemic has already led to unprecedented financial outflows from developing countries, as the U.S. dollar reasserts its role as world money. The optimisation, over decades, of the global financial system for frictionless return-seeking by mobile capital, which mostly originates from the global North, means that developing countries will be starved once again of much-needed funds. Capital controls, used sensibly, could enable more long-term investments which generate productive jobs.

Lastly, debts cannot be allowed to trump social development – not again. Indebted governments need fair debt renegotiation procedures, especially if they have accrued debts for managing the pandemic. Households which use financial services, such as microfinance, need more than good intentions, especially if they have suffered from Covid-19 or the lockdown. They deserve robust consumer protections and a fresh start if they need one.

Reasserting social control to build back better

None of these ideas are particularly radical – they used to be part of the established policy catalogue prior to financialisation – nor are they transformative in themselves. But they may offer steps toward a more fundamental reassertion of society over finance. We need to ‘build back better’ in ways that are equitable, sustainable, and democratic. This will necessarily involve mobilising financial flows, systems and institutions. We also should not have to rebuild this often. This will require much more stable, socially controlled finance.

To let unbridled financialisation continue – with more bailouts for the rich, more international financial liberalisation, more social assets gobbled up by institutional investors seeking safe havens – would merely increase our vulnerability to future shocks. It would be to ‘build back worse’. To ‘build back better’ means to de-financialise. Only a limited financial system, controlled by societies, not the other way around, is fit for purpose.

This blog post is part of a series to introduce the Business, Markets and the State (BMAS) research cluster’s Position Papers. To read the position paper on finance, please go here. To see for all the position papers here.